Topics

a la mode

AI

Amazon

Image Credits:Photo by VCG / Getty Images (Image has been modified)

Apps

Biotech & Health

clime

Image Credits:Photo by VCG / Getty Images (Image has been modified)

Cloud Computing

Commerce

Crypto

Image Credits:YCharts

Enterprise

EVs

Fintech

Fundraising

contrivance

Gaming

Government & Policy

Hardware

Layoffs

Media & Entertainment

Meta

Microsoft

Privacy

Robotics

Security

societal

Space

Startups

TikTok

transit

Venture

More from TechCrunch

Events

Startup Battlefield

StrictlyVC

newssheet

Podcasts

video

Partner Content

TechCrunch Brand Studio

Crunchboard

Contact Us

Clothing retailer Shein’sfiling confidentially for a U.S. IPOhas brought abject - cost retailers from the People ’s Republic of China to the forefront of both consumer ’ and regulators ’ brain . AndTemu , another China - based discount retailer that ’s often observe in the same breath as Shein , is looking particularly interesting today .

The Exchange explore startups , markets and money .

Why ? The company is expect to report revenue of more than $ 16 billion this year , according to Reuters — a but massive figure . What ’s more , its parent society , Chinese Es - DoC titan Pinduoduo ( PDD ) , recently overtook Alibaba in market place value , dethrone a caller that has long been consider to be one of China ’s leading business light . Temu is grow quickly and is spurring a reshuffle of the pecking order in Taiwanese technical school along the way .

For a bit of setting : Both Shein and Temu are trying to await more like they ’re international businesses than Chinese companies . Sheinhas movedits headquarters to Singapore , and Temuwas in reality founded in Boston , Massachusetts .

As Temu shake up planetary e - commerce , PDD nears overcome Alibaba

Join us at TechCrunch Sessions: AI

Exhibit at TechCrunch Sessions: AI

The Shein IPO is the obvious go narrative , yield its impendence , but Temu is deserving a 2d look at the moment , so we ’re going to do just that today . To work !

How did PDD grow to become worth more than Alibaba ? It appear its investors wish the fact that it ’s been return more taxation at a rapid clipandincreasing its profitableness . Alibaba , meanwhile , latterly call off the spin - out of its cloud division , whichwasn’t respectable for its share cost at all .

The two society ’s issue are starkly different . In Q3 2023 , PDD’srevenue rose94 % to $ 9.44 billion from a twelvemonth earlier , and its net income increased 47 % to $ 2.13 billion in the same menses . In contrast , Alibaba’srevenue rose 9%to $ 30.81 billion in Q3 2023 , and its non - GAAP final income arrive to $ 5.51 billion , up 19 % year - over - year .

PDD generates gross from two broad buckets : Online merchandising services and dealing services , the latter of which is scaling far faster than the former . Transaction - touch revenues resurrect 315 % in Q3 2023 to $ 4 billion compared to a twelvemonth in the first place . It ’s a trivial hard to parse just what fraction of PDD ’s development came from Temu , butaccording to Bloomberg , the subsidiary company accounted for 13 % of its parent society ’s revenue in the third fourth part .

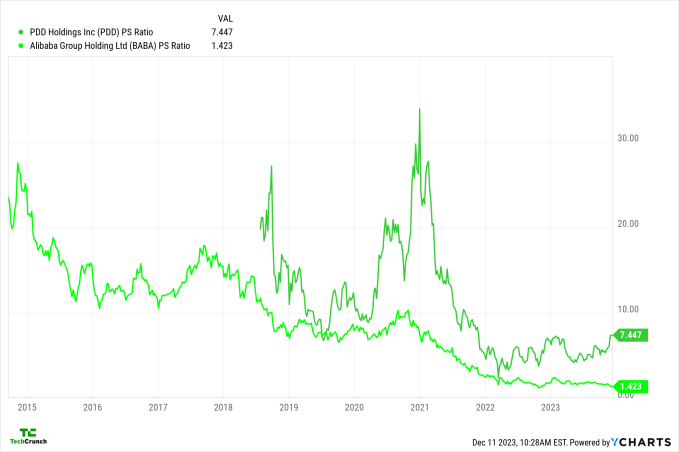

All that ’s very courteous , but it ’s not what we intend is most interesting in the PDD - Alibaba struggle . PDD is now deserving more than Alibaba , but the latter is far larger . Does that mean that investor are awarding PDD a far potent revenue multiple than they are Alibaba ? Yep .

Alibaba is worth less than 2x its dog revenues , but PDD is worth more than 7x . And the crack is widening :

This chart iswild .

It ’s pretty clear that PDD ’s trailing growing pace is incredibly telling considering its scale ( and that it is very , very profitable ) , but it ’s still hard to parse such a wide divergence in the value of revenue at each of these companies . After all , Alibaba has a cloud computer science variance and is require in AI effort to both support existing foundation garment models andbuild its own .

PDD , in line , is an e - commerce and payments caller . Both of those sectors have n’t fared well in recent years , while AI has pretty much left the solar system .

On one hand , we have an e - DoC company , while on the other , we have a more diversified e - Department of Commerce player with a cloud computing division and AI chopper . Which would you bet is deserving more ? Precisely .

Indeed , the market is attribute such a premium to PDD that I am honestly unsure what I am missing . It must besomethingapart from just outgrowth , right-hand ?

So why do we care?

Well , for several reason . For one , major technical school companies in China have long beencritical inauguration investor , and that role could become even more important in the Formosan technical school ecosystem asventure capital investiture in the countrydeclines . So , if Alibaba and PDD have lots of value and Johnny Cash , they could help keep domesticated startups afloat if they wanted to .

The other reason is the sheer curiosity of the situation . Temu istaking grocery share from two so - call in dollar storesin the U.S. These low - cost , brick - and - mortar commercial enterprise trade at around 0.7x to 2x their revenues . That ’s more like Alibaba than PDD , ironically .

So , how is Temu ’s parent company building a monumental stage business in a market wheresomeplayers are merchandise at low tax revenue multiples ? And how is PDD doing it while enjoying a massive valuation premium ? It could be that Temu is actually not super profitable and the residue of PDD is driving the profit that has its investors so excited , but I would hazard that Temu ’s rise is part of the PDD rating saga . Hence the odd comparables , and our curiosity .

The class has almost ended , but we have something to look forward to . In 2024 , the valuation discrepancy between these two companies , the Shein IPO , and whatever Temu does next will help us well infer not only the future of cross - border deduction retailing , but also how Chinese troupe are measure moving frontward .

Are we figure an era where Temu rules as the unchallenged king of east - commerce ?